| Chemical formula | AR4 GWP | AR5 GWP | |

|---|---|---|---|

| Gas | |||

| Nitrous oxide | N2O | 298 | 265 |

| Methane | CH4 | 25 | 28 |

| Carbon dioxide | CO2 | 1 | 1 |

1. Introduction

1.1 Purpose of this guide

The Ministry for the Environment supports entities taking climate action. We recognise there is strong interest, and in some cases requirements, for entities across New Zealand to measure, report and reduce their emissions. We prepared this guide to help you measure and report your entity / organisation’s greenhouse gas (GHG) emissions on a voluntary basis (see section 1.2 for important notes on this guide’s use). Measuring and reporting empowers entities to manage and reduce emissions in line with the transition to a low-emissions, climate-resilient future.

The guide aligns with and endorses the use of the GHG Protocol Corporate Accounting and Reporting Standard (referred to here as the GHG Protocol) and ISO 14064-1:2018 (see Standards to follow). It provides information about preparing a GHG inventory (How-to Guide), emission factors (sections 3–11 , and the Emission factors workbook) and methods to apply them to activity data. We have updated the guide in line with international best practice and New Zealand’s Greenhouse Gas Inventory 1990–2023 to provide new emission factors.

Numbers in the tables are largely presented to three significant figures or three decimal places, whichever is the most appropriate. Where a number is smaller than 0.001 then four or more decimal places may be shown. For your carbon inventory use the Emission factor workbook.

Most of the source data which was used in the development of these emission factors is from 2022, unless otherwise mentioned. This is done to align with New Zealand’s Greenhouse Gas Inventory 1990–2023. This contains data for the calendar years from 1990 to 2022 (inclusive). The inventory is published 15 months after the end of the period being reported on, following the United Nations Framework Convention on Climate Change (UNFCCC) reporting guidelines on annual inventories for Parties included in Annex I to the Convention. This allows time to collect and process the data and prepare its publication.

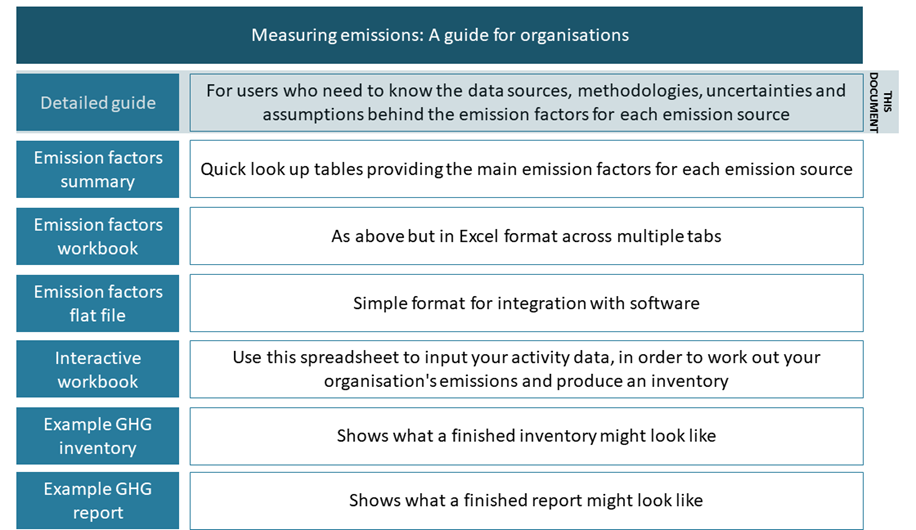

This detailed guide is part of a suite of documents that comprise Measuring emissions: A guide for organisations, listed in figure 1. The detailed guide explains how we derived these emission factors and sets out the assumptions surrounding their use. The emission factor information contained in this guide is not intended to be an exhaustively detailed explanation of every calculation performed, as this is not practical.

1.1.0.1 Feedback

We welcome your feedback on this update. Please email emissions-guide@mfe.govt.nz

1.2 Important notes

The information in sections 1 and 2 are intended as guidance only. This guidance does not replace any mandatory reporting requirements that entities may have, eg. Climate-related disclosures in line with the Aotearoa New Zealand Climate Standards (NZCS), or the Carbon Neutral Government Programme (CNGP).

Emissions factors contained within this guide may be used by entities in both voluntary and mandatory GHG inventory preparation and reporting.

The emission factors and methods in this guide are for sources common to many New Zealand organisations and support the recommended disclosure of GHG emissions consistent with the NZCS and the CNGP.

If emission factors relevant to your organisation are not included in Measuring emissions: A guide for organisations or in Auckland Council’s spend-based emissions report (see Appendix D), we suggest using alternatives such as those published by the UK Department for Energy Security and Net Zero (formerly published by the Department for Business Energy & Industrial Strategy) and the US Environmental Protection Agency (USEPA).

This guide recognises and supports the Government’s ambition for its target of Net Zero by 2050, and the many organisations that have already set, or are looking to set, ambitious emission reduction targets aligned with a science-based approach.

Measuring your emissions enables you to set reduction targets, take climate action and report quantified progress towards your goals. For support related to reaching your organisation’s targets see the Ministry’s Interim guidance for voluntary climate change mitigation.

The information in this guide is not appropriate for use in an emissions trading scheme. Organisations required to participate in the New Zealand Emissions Trading Scheme (NZ ETS) need to comply with the scheme-specific reporting requirements. The NZ ETS regulations determine which emission factors and methods must be used to calculate and report emissions.

This guide, and the emission factors and methods, are not appropriate for a full life-cycle assessment or product carbon foot printing. The factors presented in this guide only include direct emissions from activities, and do not include all sources of emissions required for a full life-cycle assessment. If you want to do a full life-cycle assessment, we recommend using life-cycle assessment databases and/or software tools. A list of relevant life-cycle inventory databases can be found on the LCANZ website.

Users seeking guidance on preparing a regional inventory should refer to the GHG Protocol for Community-scale Greenhouse Gas Emission Inventories.

Climate-related disclosures

New Zealand’s climate-related disclosure framework is made up of three climate standards, referred to as Aotearoa New Zealand Climate Standards (NZCS).

The aim is to support the allocation of capital towards activities that are consistent with a transition to a low-emissions, climate-resilient future. Climate-related disclosures are mandatory for around 200 entities in New Zealand, for reporting periods beginning on or after 1 January 2023. They include disclosure requirements covering governance, strategy, risk management, and metrics and targets. Metrics and targets have the requirement to disclose gross GHG emissions in metric tonnes of carbon dioxide equivalent (CO2-e) classified as:

Scope 1

Scope 2 (calculated using the location-based method)

Scope 3

The following information must also be disclosed in relation to the reporting entity’s GHG emissions:

a statement describing the standard or standards that GHG emissions have been measured in accordance with;

the GHG emissions consolidation approach used: equity share, financial control, or operational control;

the source of emission factors and the GWP values used or a reference to the GWP source;

a summary of specific exclusions of sources, including facilities, operations, or assets with a justification for their exclusion.

A limited number of adoption provisions apply to Scope 3 emissions.

The Aotearoa New Zealand Climate Standards and Staff Guidance for All Sectors can be found on the XRB’s website. These standards contain additional requirements, especially related to disclosures for methods, risk, reporting requirements and uncertainty management.

Carbon Neutral Government Programme

The Carbon Neutral Government Programme (CNGP) was set up by the government to accelerate the reduction of emissions within the public sector. The CNGP has published guidance for CNGP entities on measuring and reporting their GHG emissions here. It includes information on what sources of GHG emissions entities need to collect, standards to follow, methods for calculating emissions, the required information to report, who to report to, and by when.

For further guidance on this consult the CNGP website or contact cngp@mfe.govt.nz

This guide, and the emission factors and methods, are not appropriate for a full life-cycle assessment or product carbon foot printing. The factors presented in this guide only include direct emissions from activities, and do not include all sources of emissions required for a full life-cycle assessment. If you want to do a full life-cycle assessment, we recommend using life-cycle assessment databases and/or software tools. A list of relevant life-cycle inventory databases can be found on the LCANZ website.

Measuring your entity’s emissions is the first step in the journey to reducing your emissions. Developing and implementing a reduction plan is the next important step. The New Zealand Government’s first emissions reduction plan was published in May 2022. The plan is an example of a national scale plan but is not intended to provide guidance for how entities should create their own emission reduction plans. Examples of emission reduction plans published by New Zealand corporations are available online.

Measuring emissions enables you to set reduction targets, take climate action and report quantified progress towards your goals. To reach your targets see the Ministry’s Interim guidance for voluntary climate change mitigation.

Users seeking guidance on preparing a regional inventory should refer to the GHG Protocol for Community-scale Greenhouse Gas Emission Inventories.

If emission factors relevant to your entity are not included in Measuring emissions: A guide for organisations or in Auckland Council’s spend-based emissions report (see Appendix D), we suggest using alternatives such as those published by the UK Department for Energy Security and Net Zero (formerly published by the Department for Business Energy & Industrial Strategy) and the US Environmental Protection Agency (USEPA).

1.3 Gases included in the guide

This guide covers the following GHGs: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), sulphur hexafluoride (SF6), nitrogen trifluoride (NF3) and other gases (eg, Montreal Protocol refrigerant gases or medical gases).

Global Warming Potential (GWP) is an index to translate the level of emissions of various gases into a common measure, in order to compare the relative radiative forcing of different gases. GWPs are calculated as the ratio of the radiative forcing that would result from the emissions of one kg of a greenhouse gas, to that from the emission of one kg of carbon dioxide over a period of time (usually 100 years).

GWPs are applied to the non-CO2 gases to enable meaningful comparisons among the gas types compared with CO2. Where GWPs are applied to these gases, GHG emissions are commonly expressed as their carbon dioxide equivalent or CO2-e. The larger the GWP, the more a given gas warms the earth compared to CO2 over that time period. The time period usually used for GWPs is 100 years to align with UNFCCC greenhouse gas inventory reporting requirements. This is used throughout the guide.

To do this, the emissions for each non-CO2 gas is multiplied by its 100-year time-horizon GWP (GWP100) value – see Table 1. The IPCC provides more information on how these factors are calculated.

Throughout the guide, kilograms (kg) of methane and nitrous oxide are reported in kg CO2-e by multiplying the actual methane emissions by the GWP of 28 and actual nitrous oxide emissions by the GWP of 265, as per Table 1.

The GWP index value depends on two things: how effective the gas is at trapping heat while it’s in the atmosphere, and how long it stays in the atmosphere before it breaks down. For example, methane (CH4) breaks down relatively quickly, the average methane molecule stays in the atmosphere for around 12 years. On the other hand, CH4 traps heat more effectively than CO2, which has a much longer lifetime.

Changes in GWP values can be due to updated scientific estimates of the energy absorption, lifetime of the gases, or to changing atmospheric concentrations of GHGs that result in a change in the energy absorption of an additional tonne of emitted gas relative to another.

The change introduced in the previous edition from AR4 to AR5 GWPs may cause a significant change in some entities’ inventories, including those that use large quantities of refrigerants, or that use emission factors with relatively high contributions of methane. For those that see increases or reductions in their footprints, it would be misleading to interpret this as a true increase or reduction.

Table 1.1 shows the GWPs for nitrous oxide and methane comparing AR4 and AR5 values. The GWP of nitrous oxide has decreased by 11.1 per cent and the GWP of methane has increased by 12 per cent. AR5 GWPs for other gases such as refrigerants are shown in Table 7

1.3.1 Kyoto and Montreal protocols and Paris Agreement

The Kyoto Protocol, adopted in 1997, operationalised the UNFCCC by committing developed country parties to limit and reduce GHG emissions in accordance with agreed individual targets. It includes the following gases: CO2, CH4, N2O, HFCs, PFCs, SF6 and NF3.

The Montreal Protocol, adopted in 1987, is an international environmental agreement to protect the ozone layer by phasing out production and consumption of ozone-depleting substances (ODS). The Montreal Protocol includes chlorofluorocarbons (CFCs), hydrochlorofluorocarbons (HCFCs), hydrobromofluorocarbons (HBFCs), methyl bromide, carbon tetrachloride, methyl chloroform and halons. New Zealand prohibits imports of CFCs and HCFCs as part of our implementation of the protocol.

Many of the ozone depleting substances controlled by the Montreal Protocol are also powerful greenhouse gases. This, together with the 2016 Kigali Amendment of the Montreal Protocol to include the phase-down of HFCs, means it has a significant role in mitigating climate change.

The Paris Agreement, adopted in 2015, commits Parties to the agreement to put forward their best efforts to limit global temperature rise through nationally determined contributions (NDCs), and to strengthen these efforts over time. From 2024 onwards, New Zealand’s Greenhouse Gas Inventory reports under the Paris Agreement will apply the 100-year time horizon GWPs from the IPCC’s AR5.

1.4 Uncertainties

ISO 14064-1:2018 and the GHG Protocol require consideration of uncertainty: in particular, assessing and disclosing uncertainty associated with a GHG inventory.

Compared with financial accounting, carbon accounting operates in a more unpredictable, dynamic and complex environment, where uncertainty is a known and accepted concept.

Uncertainties associated with GHG inventories can be broadly categorised as scientific uncertainty and estimation uncertainty.

Scientific uncertainty arises when the science of the actual emission and/or removal process is not completely understood. Quantifying such scientific uncertainty is extremely challenging and is likely beyond the capability of most entity inventory programmes.

Estimation uncertainty arises any time GHG emissions are quantified and can be classed as either model uncertainty or parameter uncertainty. Model uncertainty refers to the uncertainty associated with the mathematical equations and models used to characterise the relationship between activity data and emissions. Parameter uncertainty refers to the uncertainty associated with the assumptions used and the activity data. Entities that choose to investigate uncertainty in their emission inventories will focus on the latter.

The following approach is used to disclose uncertainty, in order of preference.

Disclose the quantified uncertainty of the data, if known.

Disclose the qualitative uncertainty if known based on expert judgement from those providing the data.

Disclose the uncertainty ranges in the IPCC Guidelines if provided.

Disclose that the uncertainty is unknown.

1.5 Standards to follow

We recommend following ISO 14064-1:2018 or the GHG Protocol and this guide is written to align with both. Depending on your intended final use and users, we recommend downloading the relevant standards and using them in tandem with this guidance:

ISO 14064-1:20181 is shorter and more direct than the GHG Protocol. A PDF copy can be purchased.

The GHG Protocol2 gives more description and context around what to do to produce an inventory. It is free to download. The Corporate Value Chain (Scope 3) Accounting and Reporting Standard is also available. It is a guide for companies to assess their entire value chain emissions impact and identify where to focus reduction activities.

These standards provide comprehensive guidance on the core issues of GHG monitoring and reporting at an organisational level, including:

principles underlying monitoring and reporting

setting entity / organisational boundaries

setting reporting boundaries

establishing a base year

managing the quality of a GHG inventory

content of a GHG report.